Winning an SBIR Phase II award is a huge milestone, but it shifts your company from a "research lab" mindset to a "regulated government contractor" reality. The administrative burden triples: you are now facing Agency-specific budget rules, DCAA audit requirements, and complex tax implications like Section 174.

The "regulatory environment" isn't a single set of rules—it varies wildly depending on whether your funding comes from a Contract Agency (DoD, NASA) or a Grant Agency (NIH, NSF, DOE).

In this guide, we break down exactly how to manage these requirements without drowning in paperwork or risking unallowable costs.

Phase II Budgets: The "Safe Rate" Trap

Creating a Phase II budget is common ground for all agencies, but the limitations on that budget are where companies lose money.

1. The "Safe Rate" Explained

Agencies like NIH and NSF offer a "Safe Rate"—essentially a standard indirect rate (often 40% of Direct Salaries) you can use without providing detailed financial proof.

- The Trap: If your actual indirect costs (overhead, rent, G&A) are higher than the Safe Rate, you are paying those expenses out of your profit. You cannot bill the government for them.

- The Fix: If your real rates are higher, do not settle for the Safe Rate. Negotiate a Negotiated Indirect Cost Rate Agreement (NICRA). It requires more documentation, but ensures full cost recovery.

2. Budget Input Platforms

Be prepared for the specific portal headaches:

- DoD: Uses the Defense SBIR/STTR Innovation Portal (DSIP).

- Grants: Uses Grants.gov / Workspace.

Tip: Ensure your SAM.gov registration is active weeks before these deadlines. A lapsed SAM account will block your submission instantly.

Award Negotiations & DCAA Compliance

Once selected, the scrutiny begins. This is often the first time a small business encounters the Defense Contract Audit Agency (DCAA).

The SF1408 Pre-Award Survey

If you are awarded a Cost-Plus contract (common in DoD), the DCAA will perform a Pre-Award Survey of your accounting system (Standard Form 1408).

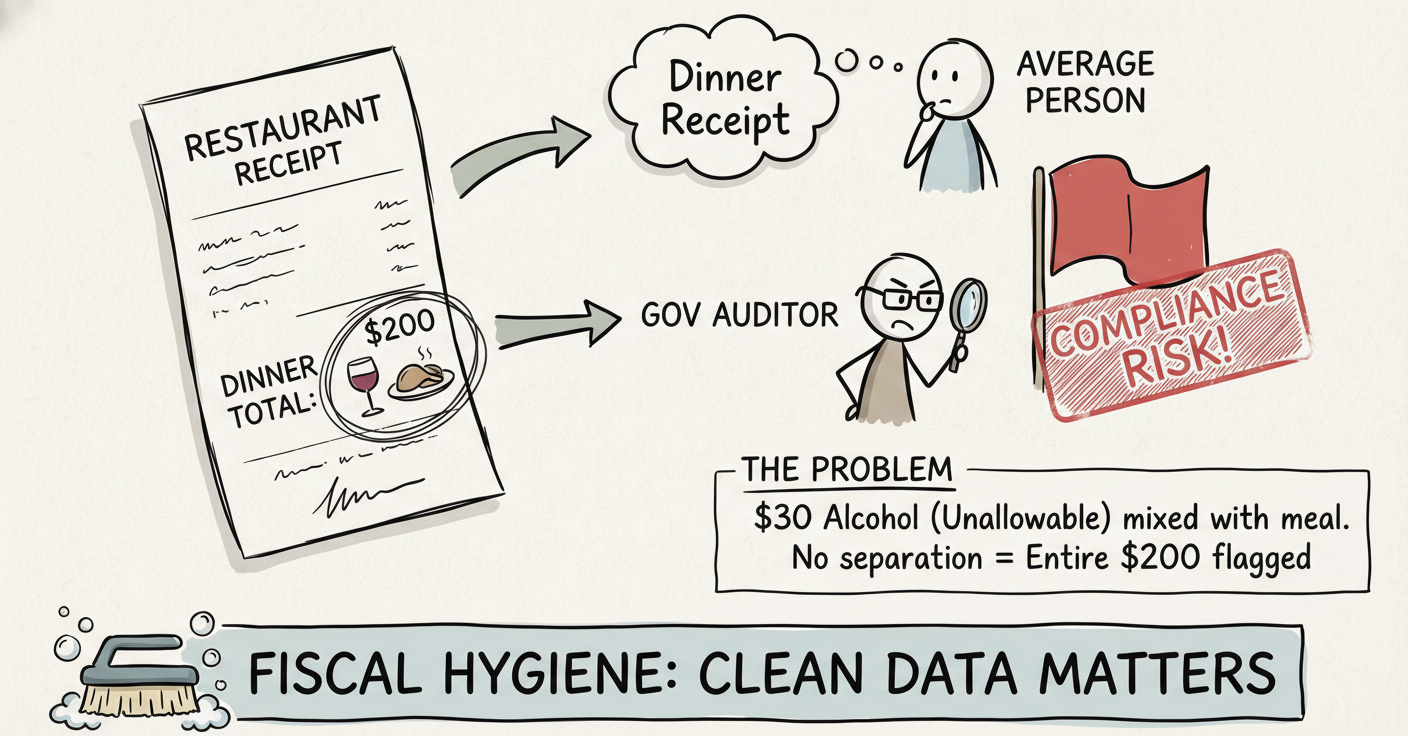

- They are checking for Segregation of Costs: Can your system distinguish between Direct costs (billable) and Indirect costs (overhead)?

- They are checking for Unallowable Costs: Does your system automatically filter out costs like Alcohol (FAR 31.205-51) or Interest (FAR 31.205-20)?

NSF CAP Review

The National Science Foundation (NSF) has its own version called the Cost Analysis and Pre-Award (CAP) review. It is just as data-intense as a DCAA audit. Do not underestimate it.

Getting Paid: Invoicing & Financing

Cash flow is king. Understanding how to bill is critical for survival.

DoD Contracts (WAWF)

- Method: Cost-Plus or Fixed Price.

- System: Wide Area Workflow (WAWF) / PIEE.

- Risk: In Cost-Plus contracts, you bill "Provisional Rates." If your actual rates at year-end are lower, you owe the government money back.

Grants (Drawdown)

- Method: Drawdown from the U.S. Treasury (PMS - Payment Management System).

- System: ACM$ (NSF) or PMS (NIH).

- Exception: NSF Phase II grants are often "Fixed Amount," where you draw down purely based on milestones, not detailed costs incurred.

Audits & Reporting: The Incurred Cost Proposal (ICP)

If you have a cost-reimbursable contract, your financial year doesn't end on Dec 31st. It ends when you submit your Incurred Cost Proposal (ICP)—usually due 6 months after fiscal year-end.

- What is it? A "true-up" calculation comparing the provisional rates you billed vs. your actual rates.

- Who audits it? DCAA.

- Threshold: If you have over $250M in reimbursable costs (rare for SBIR), it's mandatory. For smaller firms, DCAA risk-assesses you.

Audit Trigger: Frequent corrections to your invoices or a messy SF1408 survey increase your "Audit Risk" score, making a full standard audit more likely.

Taxes: The Section 174 Nightmare

Warning: Since 2022, IRS Section 174 requires businesses to amortize R&D expenses over 5 years (15 years for foreign research), rather than deducting them immediately.

- Impact: You may have a massive taxable "profit" on paper, even if you spent all your cash on research.

- Action: Consult an R&D tax specialist. You must plan for this tax bill.

Visual Content Opportunities

Recommendation 1: A "Compliance Timeline" infographic showing the journey from Phase I Award -> Phase II Selection -> SF1408 Audit -> First Invoice -> Annual ICP. Alt Tag: Timeline of SBIR Phase II compliance milestones including DCAA audits and Incurred Cost Proposals.

Recommendation 2: A bar chart comparing "Safe Rate" vs. "Negotiated Rate" recovery, visually showing the lost revenue when actual costs exceed the safe cap. Alt Tag: Comparison of SBIR Safe Rates versus Negotiated Indirect Rates showing potential profit loss.

Frequently Asked Questions

Do I need an audit if I have a Grant?

Generally, no DCAA audit for grants. However, if you expend more than $750,000 in federal funds in a year, you trigger a Single Audit (formerly A-133 audit) by an independent CPA firm.

What happens if I overbill my indirect rates?

You must pay it back. This is why monitoring your rates monthly is critical. If you bill 50% overhead but your actuals are 40%, you will owe the difference to the government after your Incurred Cost Proposal is settled.

Can I do this all in Excel?

For Phase I? Maybe. For Phase II Cost-Plus? No. The risk of manual error is too high, and DCAA auditors are skeptical of Excel-based "systems" for calculating indirect rates. You need a systematized General Ledger.

Phase II Compliance, Solved.

Stop worrying about "Safe Rates" and unallowable costs. AudCor's Zero Effort Compliance platform continuously scans your books to keep you audit-ready, so you can focus on the R&D.

DCAA-Ready. Secure. Automated.